At the same time, I regard debt sustainability, in the broad sense, as one of the major financial stability risks on either side of the Atlantic. And rising interest rates have brought this vulnerability to the surface.

There is no linear correlation between the two – here at the ESM I do not have to belabour the point made by Dornbusch and others that markets can regard debts as sustainable for quite some period of time, before they no longer do. Such potential non-linearities call for additional caution.

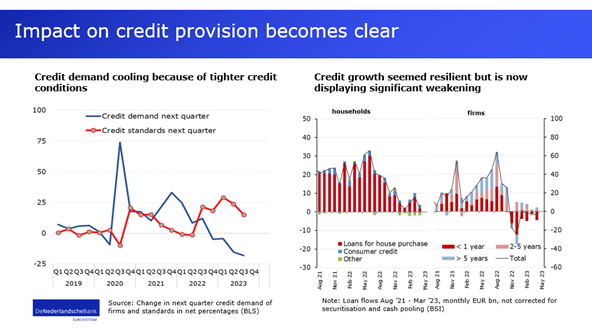

Households are experiencing a real income squeeze, which compromises their debt servicing capacity. Though some can benefit from having fixed their borrowing costs at extended maturities during the low-for-long era, this only partially and temporarily cushions the blow.

And non-financial corporates face a similar situation. In the Netherlands, for example, 38 percent of total debt of non-financial corporates will mature within the year or will have to be refinanced at a likely higher interest rate. Higher interest expenditures might eventually also trigger some corporate liquidity issues.

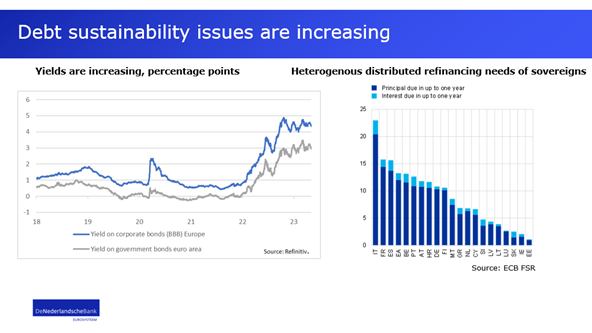

And alongside households and non-financial corporates, the debt sustainability of euro area sovereigns is also affected by the recent rise in bond yields. Here too, the low-for-long era has partially been locked-in with fixed borrowing rates spanning a relatively long horizon. But this can only buy time rather than obviate the inevitable adjustment in the primary fiscal balance.

So I urge caution.

Even though our financial system has proven its resilience, largely due to the buffers we have built since previous crises, and even though we have weathered the shocks of recent years, we mustn’t be complacent. Building resilience does not prevent shocks from happening. It just helps us to deal with them.

So it is encouraging that we as central bankers, in deciding on our course of action, have started to pay more attention to the interplay between monetary policy and financial stability. Monetary policy affects the stability of the financial system. But in turn, we need a stable financial system to effectively transmit monetary policy. Financial stability is a pre-requisite for medium-term price stability.

And as Chair of the Financial Stability Board, I must underscore that a stable financial system is also a goal to be pursued in its own right.

So where does that leave us?

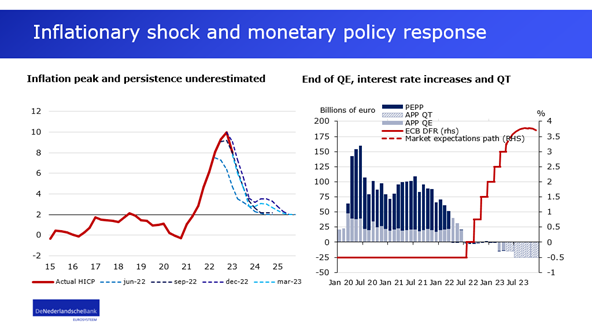

Central bankers will have to continue tightening monetary policy for as long as necessary, until we see inflation return to our two percent target over the medium term.

But we will do this step by step. Because the tighter monetary policy gets, the more forceful its transmission to output and prices that is still largely in the pipeline. And with each step, the financial system will have to continue adjusting to the higher interest rate environment. The recent financial turmoil on the other side of the Atlantic illustrates that this cannot be taken for granted.

And with each step, we continuously learn from our experiences.

Allow me to share with you two valuable lessons we have learned in recent years. Lessons that will help us walk this tight rope – step by step. Lessons that will help us tackle future challenges – and go from one concrete achievement to the next.

A first lesson from the recent episode is that the so-called separation principle can be maintained for longer than some might have expected. According to this principle, a central bank should clearly separate its function as lender of last resort from its function as monetary policy maker.

Since the Global Financial Crisis, policy makers worldwide have become more experienced and more innovative with various forms of lending operations. With this experience came a more coherent and powerful toolkit. A toolkit that can, and in my view should, be used to adhere to the separation principle for as long as possible.

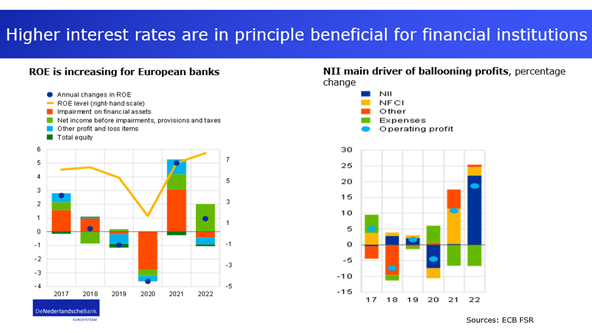

Against the backdrop of a better regulated and better capitalised financial system, we can now deal with a broad range of financial stability related risks without compromising on medium-term price stability.

The second lesson we have learned, is that moderate and contained levels of financial turbulence do not necessarily have to be at odds with medium-term price stability. Repricing of risk in financial markets can contribute to tighter financial conditions for a given policy rate. Monetary policy normalisation also entails a reduction of the central bank footprint in financial markets, a decompression of term premia, and some repricing of risks. As long as such repricing is not excessive, it can in fact be combined with a somewhat lower terminal policy rate that would still be compatible with medium-term price stability.